No risks and sky-high returns are the two things that an investor looks for while thinking of investing their money. However, you must know that these two can’t co-exist. Wherever there would be high returns (stocks), there would be more risks of losing money.

Nevertheless, you can always analyze your risk-taking ability and get set to multiply your money.

Let’s see the investment options available.

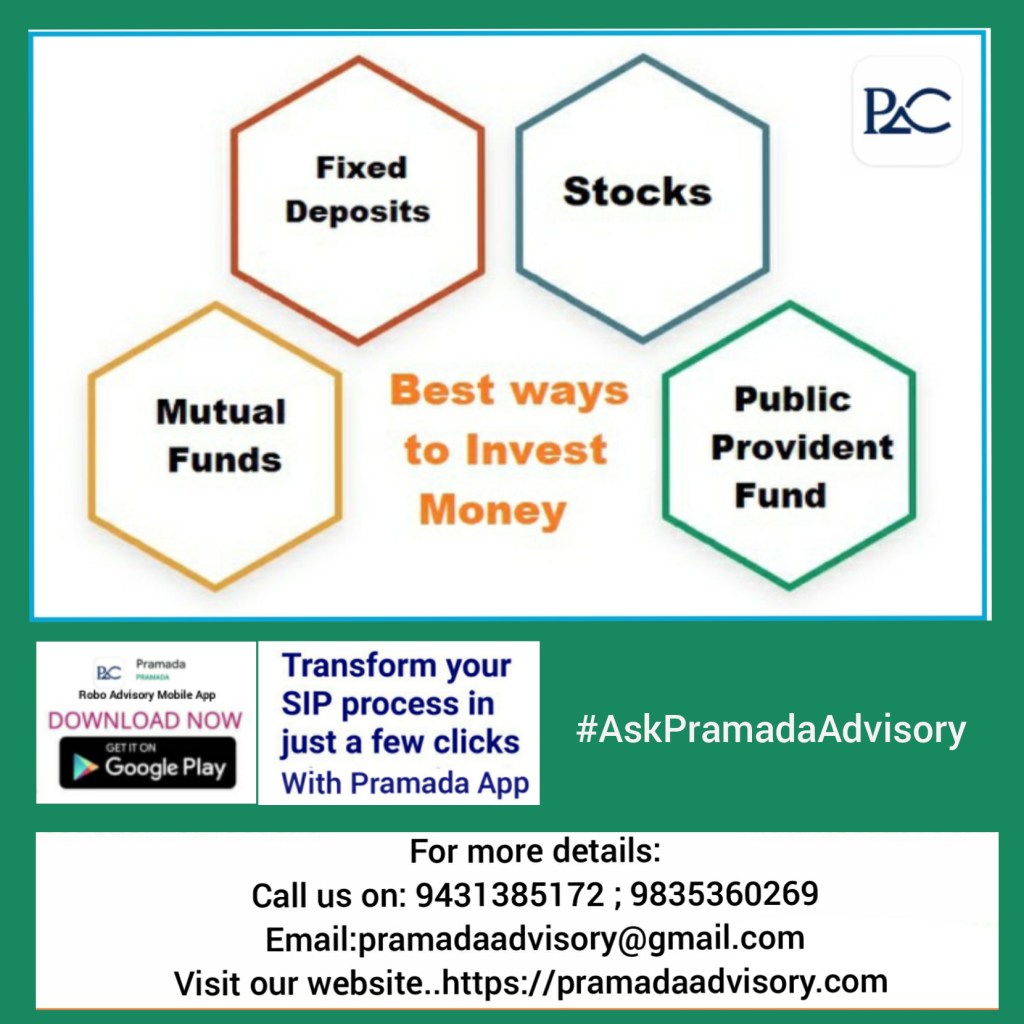

The top investment options in India are divided into two categories:

1. Financial

These are market-linked and fixed income investments. For example, stocks, mutual funds, fixed deposits, public provident fund, etc.

2. Non-financial

These may include gold and real estate.

Here are the top investment options in India that can help you reach your financial goal.

- Fixed Deposits

This is the most secure option. You can transfer some of your savings to a fixed deposit at a bank of your choice and enjoy monthly, quarterly, yearly, etc. interest on your deposit.

- Stocks

The volatility of the market can both yield high returns on the money invested, as well as losses in case of predictions going wrong. However, if you keep the money invested for a while, and choose stocks of a good stability and quality, equity is usually able to deliver equivalent or even more returns in the future. However, you must refrain from investing in risky stocks at this time of the COVID-19 pandemic, considering how volatile the market is.

- Senior Citizens Savings Scheme

If you’re above 60, this is the best scheme for you. It has a five-year tenure, with an upper limit of investment at a good Rs 15 lakhs. You get the interest on the amount every three months till the amount matures.

These are a few of the best investment schemes in India. Try them out. But ensure that you’ve consulted a financial expert.

In case you need personalised investment advise on which particular funds / schemes to choose, you can drop an email or whatsApp to me