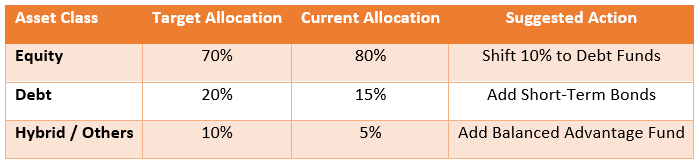

Over time, some funds may out perform and others may lag, causing your portfolio to drift from its intended asset allocation. This can alter your overall risk profile.

Smart Move:

Review your portfolio annually to evaluate fund performance, goal alignment, and asset allocation. If equity exposure increases beyond your comfort zone, rebalance by shifting a portion to debt or hybrid funds.

Illustration:

Takeaway:

Regular reviews ensure your investments stay aligned with your financial objectives — not just market trends.

👉 Get in touch with us today to schedule a personalized portfolio review and take the next step toward long-term financial growth.

Download our Pramada mutual fund app & start investing for your long-term financial goals.

Mutual Fund investment are subject to market risks read all documents carefully before investing.

If you are asked if you get a chance to invest in 2005, will you invest? Almost everyone will have the answer – yes, and if we had the opportunity, we would have sold everything we would have put in equity.

But as soon as it comes to investing in equity for the next 10 to 20 years from today, the answer changes….

The market is risky right now, let’s stop a little.

There may be a recession ahead, gold is right. There are many other reasons to avoid equity.

Imagine how many times the market fell after 2005. The 2008 recession, 2020’s corona crash and many ups and downs in between but despite this, the returns of the last 20 years have been fantastic.

So why not the next 20 years?

India’s economy today is stronger than ever before. Yes, corrections will keep coming in between, but in the long term equity will give you real growth.

Trust and stay tuned. That is the biggest key to investment.

Happy Investing!

“We create the link between your needs and Solutions”

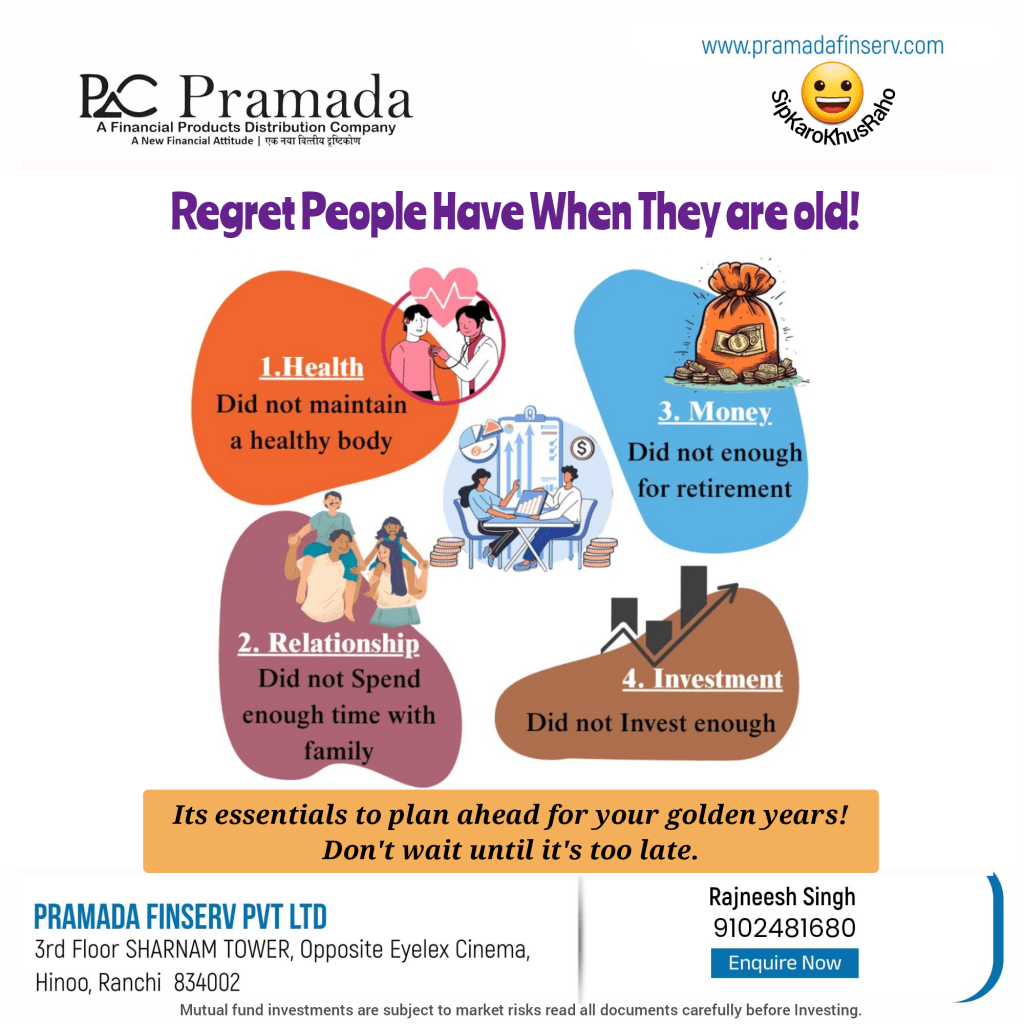

I had an acquaintance. It was his dream to retire at the age of 50. He had set a target corpus of ₹ 8 crore.

Discipline and hard-earned invested, and by the age of 49 his portfolio reached ₹ 7 crore. That is, the target was almost complete. But sadly, he died before he saw him at age 50.

Many of us devote a large part of our lives to planning to add money.

“We need so much corpus” “We need so much SIP.” “We need so much retirement funds”

But no one thinks that there is no guarantee of life.

What is real investment?

Health – Don’t forget health while making money.

Family time – Numbers will keep increasing, but moments spent together will never come back.

Balance – Save money, but don’t forget to enjoy it.

The real purpose of wealth is not just to create portfolios, but to improve life and relationships.

So planning money is important, but planning to live with it is equally important.

Remember the Simple Line: “Wealth is meaningless if you don’t have time to live it.”

The job of the media is to make noise, especially when the market goes down a bit. Every fall is made breaking news, and every fluctuation is shown as a crisis.

But sensible investors know that this is the nature of the market.

The market never goes straight. Fluctuations are part of this. If you react to every news item, you’re not investing, you’re pursuing fear.

That is why discipline is most essential. Stay calm, focus on basic things, remember your long-term goals, stay away from noise. If there is still panic, it is better to talk to a trusted financial advisor who helps you wisely, not in emotions.

Investing is a journey. It will determine your patience, not the headline of the newspaper.

हर कोई पैसा कमाने की बात करता है। अमीर लोग वास्तव में ऐसा करते हैं लेकिन एक सटीक योजना के साथ। इस पोस्ट में बताया गया है कि कैसे अमीर भारतीय वास्तव में करोड़ों कमाते हैं ….

इसकी शुरुआत दो तरह की पूंजी से होती है:

1.मानव पूंजी (Human Capital)- आपका कौशल, ज्ञान, प्रयास

मध्यम वर्ग केवल मानव पूंजी पर निर्भर करता है लेकिन करोड़पति दोनों बनाते हैं।

फिर आता है कैश फ्लो : ……. आप जो कमाते हैं = जिसे आप नियंत्रित कर सकते हैं।

अमीर लोग अपनी आय का उपयोग कैसे करते हैं: …..

– 50%: खर्च (आवश्यकताओं पर, इच्छाओं पर नहीं)

– 10%: बचत (आपातकालीन भंडार बनाएँ)

– 40%: निवेश करें (हर एक महीने)

40 प्रतिशत से अधिक निवेश नियम वह जगह है जहाँ वास्तविक खेल शुरू होता है। दो तरह के निवेश रास्ते हैं : ….

1. सक्रिय निवेश (Active Investing) – में आप खुद शोध करते हैं। आप जोखिमों का प्रबंधन करते हैं। ये उद्यमियों, स्टॉक-पिकर्स, रियल एस्टेट खिलाड़ियों द्वारा उपयोग किया जाता है। इसमें शामिल हैं: – स्टॉक – रियल एस्टेट – क्रिप्टो – छोटे व्यवसाय – सोना।

इसके लिए समय, प्रयास और भावनात्मक शक्ति की आवश्यकता होती है।

2. निष्क्रिय निवेश ( Passive Investing)– में आप सिस्टम या विशेषज्ञों को अपने लिए काम करने देते हैं। वेतनभोगी पेशेवरों और व्यस्त निवेशकों द्वारा उपयोग किया जाता है। इसमें शामिल हैं: – म्यूचुअल फंड – इंडेक्स फंड (जैसे निफ्टी 50, सेंसेक्स) – आरईआईटी ( REITs)- ईटीएफ में एसआईपी – पी2पी लेंडिंग।

इसे शुरू करना आसान है। एक बार जब आप कंपाउंडिंग देखते हैं तो इसे रोकना मुश्किल होता है।

* रहस्य (The Secrets )? अमीर भारतीय या ये और या वो का चयन नहीं करते हैं – वे दोनों का चयन करते हैं।

सक्रिय (Active) = उच्च रिटर्न, अधिक नियंत्रण

निष्क्रिय (Passive) = स्थिरता, शांति से सोना

* वास्तविक गणित (Real Math): 13% CAGR पर 20 वर्षों के लिए ₹5,000/माह का निवेश करें = ₹1 करोड़+

यह कोई जादू नहीं है। यह अनुशासन + समय + भारत की विकास कहानी है।

क्या आप अपनी निवेश यात्रा शुरु करना चाहते हैं या उसे बेहतर बनाना चाहते हैं? अपने लक्ष्यों और जोखिम उठाने की क्षमता के अनुरूप एक व्यक्तिगत निवेश रणनीति के लिए प्रमादा फिनसर्व के साथ जुड़ें।

Investing systematically is a prudent way to manage finances and build wealth over time.

In the realm of mutual funds, three popular systematic plans are SIP (Systematic Investment Plan), SWP (Systematic Withdrawal Plan), and STP (Systematic Transfer Plan).

Each serves distinct purposes and caters to different financial needs.

Here’s a detailed look at each plan …

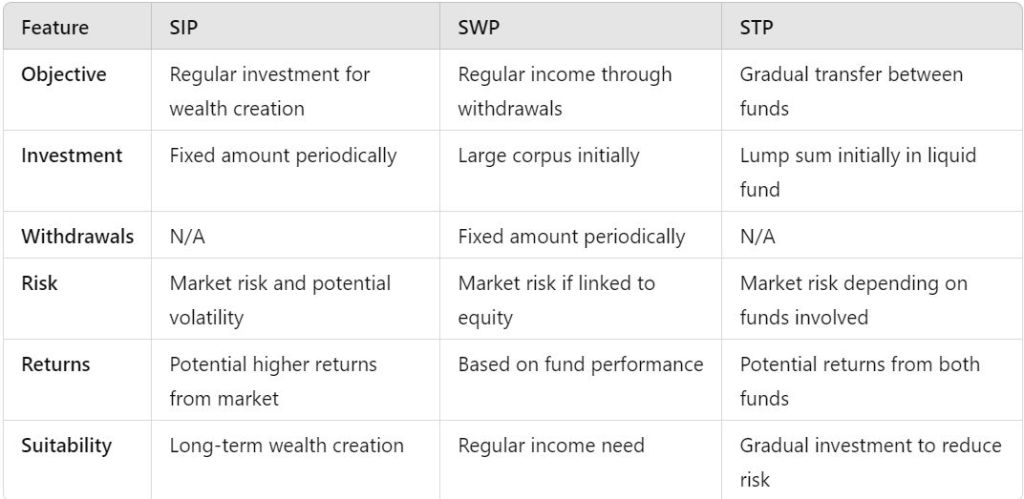

Systematic Investment Plan (SIP):

Definition:

A disciplined approach to investing a fixed amount in a mutual fund at regular intervals (e.g., monthly).

How It Works:

– Regular investments regardless of market conditions. – Purchases more units when the market is low and fewer units when the market is high, averaging the cost over time. – Encourages disciplined investing and benefits from compounding.

Example:

Invest Rs. 5,000 every month:

– NAV is Rs. 20: Units bought =5,000/20=250

– NAV is Rs. 16: Units bought =5,000/16=312.50

In this way, units are accumulated by periodically running the NAV of the Fund.

Benefits:

– Easy to invest and monitor. – Suitable for long-term goals. – Compounding enhances growth.

Systematic Withdrawal Plan (SWP):

Definition:

Allows you to withdraw a fixed amount from your mutual fund at regular intervals.

How It Works:

– Invest a large corpus initially. – Withdraw a fixed amount periodically (e.g., monthly) to generate regular income.

Example:

-Invest Rs. 10 lakhs in a debt mutual fund, and withdraw Rs. 10,000 monthly.

Benefits:

– Provides steady income. – Suitable for retirees or those needing regular cash flow. – Flexible withdrawal options.

Systematic Transfer Plan (STP):

Definition:

Transfers investments from one mutual fund scheme to another within the same fund house.

How It Works:

– Invest a lump sum in a liquid fund. – Transfer a fixed amount regularly to an equity fund to mitigate risk.

Example:

– Invest Rs. 5 lakhs in a liquid fund, transfer Rs. 50,000 monthly to an equity fund.

Benefits:

– Gradual investment in equity reduces risk. – Earn potential returns on both source and target funds.

Is it strong or not? Is it right for the weather? Is the price okay?

The real test begins when a storm hits the sea:

Is it nervous or quiet? Does direction change or persist? Does fear return to the shore or move forward with risk? Does the journey complete?

Have you invested in SIP!

How much research you do,the real game is in the face of market fluctuations. Fear, greed, or discipline, is what determines your behavior as whether you win or lose.

The boat needs to be good, but the sailor’s courage and acumen matter more than that.

Investing is important thoughtfully, but investor patience and discipline are more important than that.